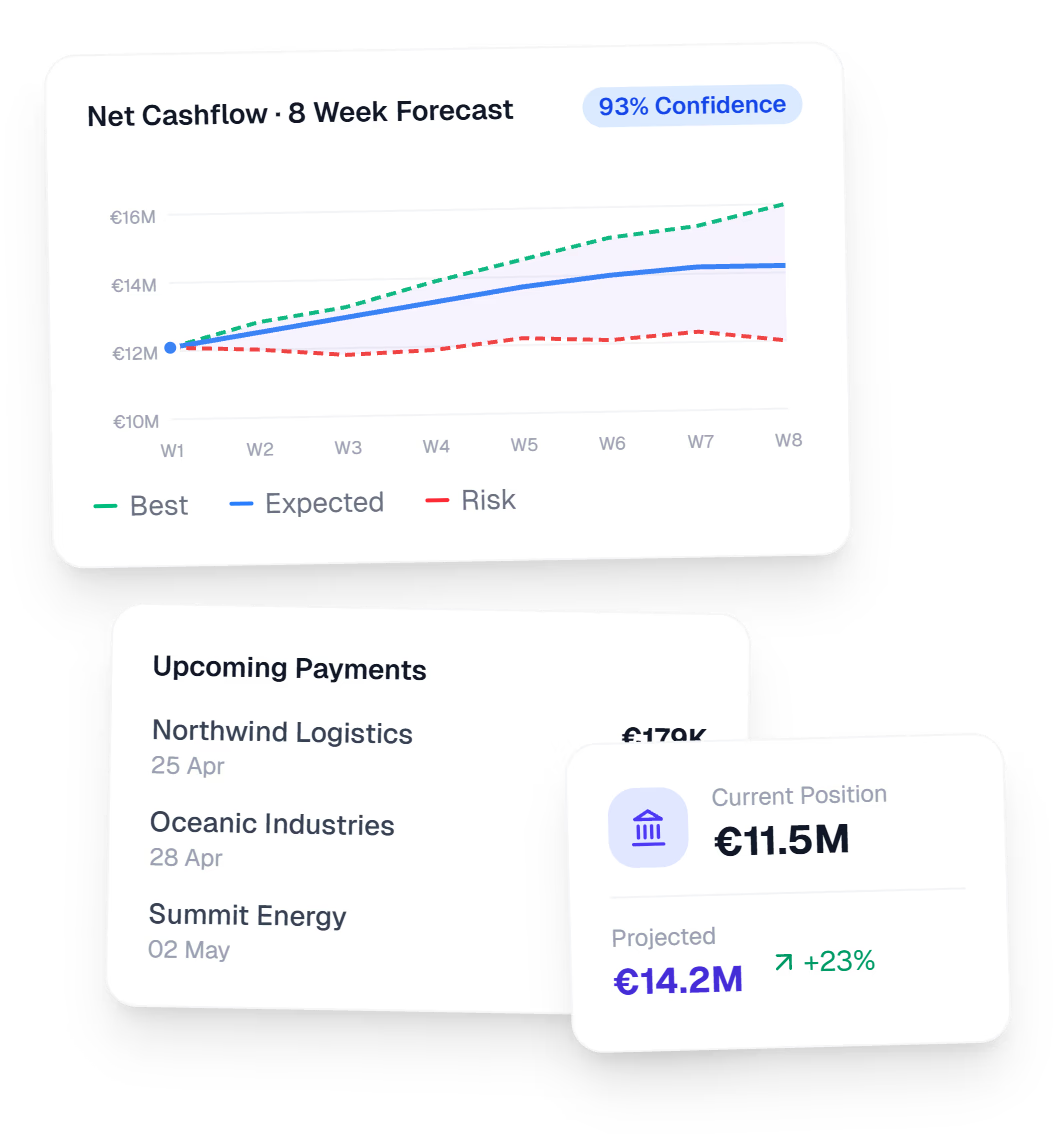

Multi-horizon net cash forecasts from live AR and AP data. 90 to 95 percent accuracy out to 90 days. Confidence ranges, not single-point guesses. Full-year horizons for FX-exposed portfolios.

Legacy tools run a single auto-regressive model for every customer and horizon. CashPulse picks the right architecture per region, entity, and forecast window. Quantile outputs and external signal ingestion as first-class inputs.

Auto-regressive for stable short cycles, behaviour-driven ML for mid-horizon, deep learning for long-cycle FX or commodity-exposed portfolios.

Every forecast ships with three lines: best-case P90, expected P50, and risk-adjusted P10. Confidence bands, not deceptive single numbers.

Multi-dimensional pattern matching with persistent memory. Captures customer behaviour and external signals legacy auto-regression cannot see.

Hundreds of model configurations trained in parallel. The champion model is selected automatically based on accuracy and stability. Forward-looking factors like FX, commodity prices, weather events, and economic indicators feed the engine.

Hundreds of configurations tested simultaneously per portfolio. The right model wins on the data, not on assumptions.

Per-horizon accuracy across 7, 30, 90, and 365 days, forecast bias, and per-customer hit rate measured continuously. Best model wins.

Weekly retraining cycles. When accuracy drops below threshold, the engine rebuilds before treasury notices.

Traditional forecasts look backward at aging buckets and bank snapshots. CashPulse aggregates live AR data, payment predictions, and external signals into scenario-based net cash curves by entity, currency, and category.

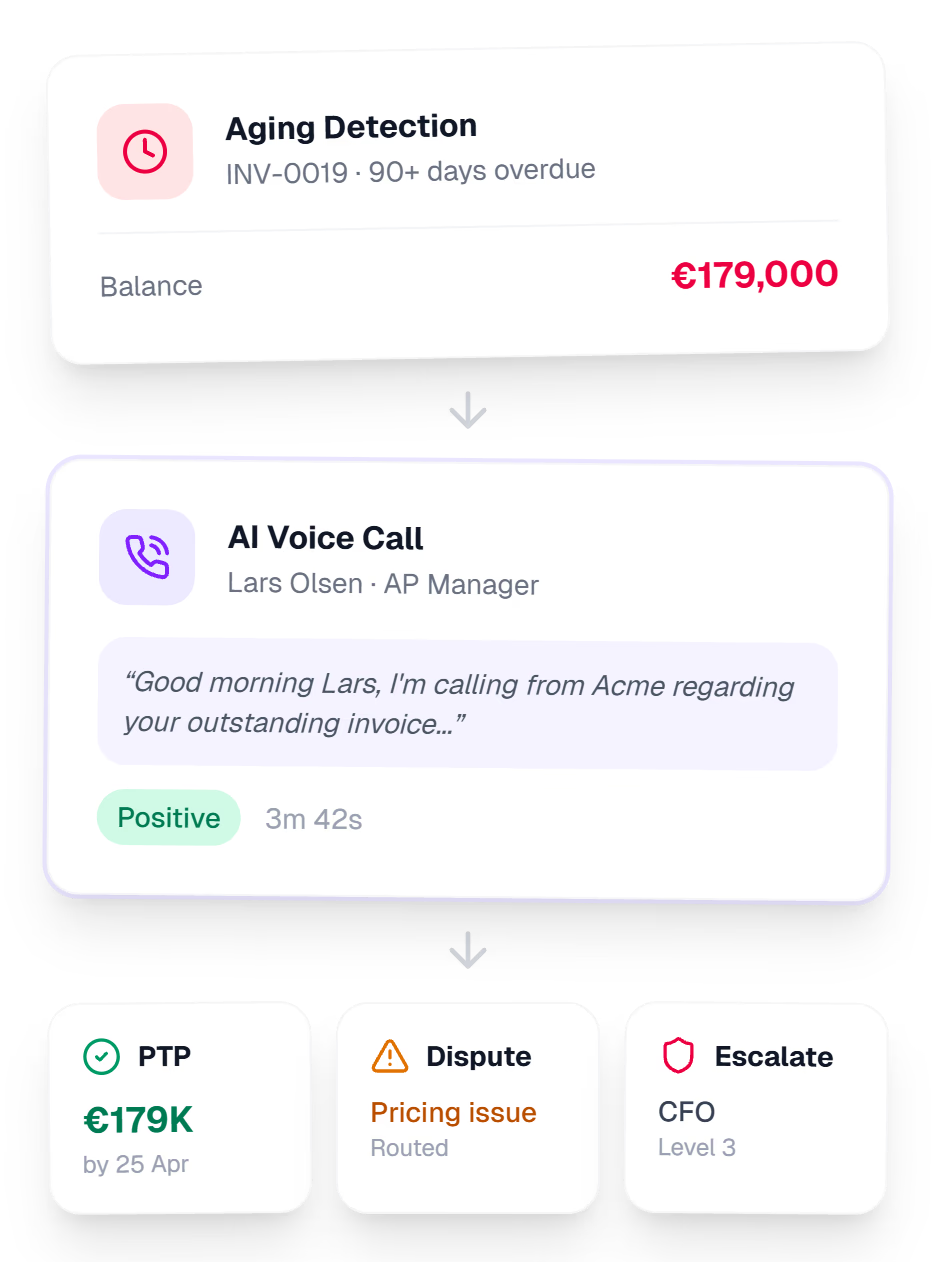

Matched payments from ClearMatch, active disputes from ClaimIQ, promise-to-pay dates from CollectPulse. Committed POs, payroll, tax schedules. Not aging buckets.

FX rates, commodity prices, weather events, harvest cycles. Forward-looking factors that materially shift when customers pay.

Each entity's flow netted at the legal-entity level with intercompany flows eliminated. Treasury teams see net cash, not gross inflows.

Start from AI-predicted baselines, then layer custom assumptions like FX changes, payment delays, and seasonal adjustments. Real-time credit risk scoring flags breaches before they happen, not after.

Layer FX shifts, payment delays, and seasonal adjustments on top of AI baselines. Compare base, optimistic, and stress scenarios side by side.

Plan against P10 for liquidity floors and covenant compliance. Stress-test by adjusting external inputs and watch the confidence band move.

Real-time customer scoring combining payment behaviour, credit utilisation, external ratings, and AI-predicted trends. Flag breaches before they happen.

Three steps. Fully automated. Daily refresh.

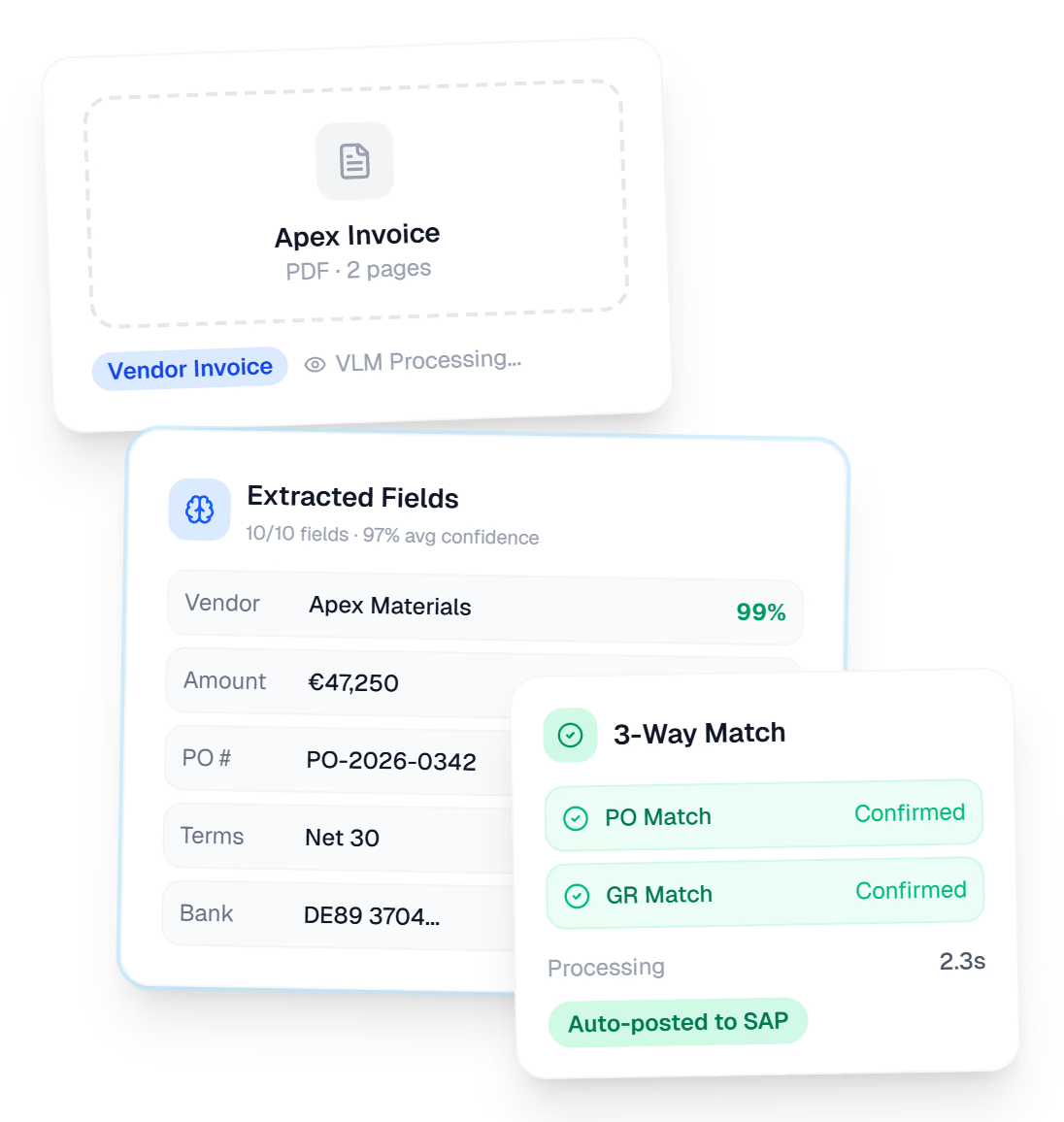

Plug into your ERP, bank feeds, and external data sources. CashPulse ingests live AR data, payment history, AP commitments, and market signals.

Hundreds of model configurations tested in parallel. The champion model is selected automatically based on accuracy and stability.

Rolling 30, 90, and 365-day forecasts with confidence bands, payment-level predictions, and scenario overlays. Updated daily.

30, 90, and 365-day rolling forecasts updated daily from live AR and AP data, payment patterns, and external signals like FX and commodity prices.

Meet ClearMatch →Layer custom assumptions on top of AI baselines. Compare base, optimistic, and stress scenarios in one view with action-linked outcomes.

See how Vero acts on scenarios →Real-time risk assessment per customer combining payment behaviour, utilisation, and predicted trends. Flag breaches before they happen.

See CollectPulse →Consolidated forecasts across entities, currencies, and ERPs in reporting currency, with drill-down to individual forecasts and customers.

Meet Vero →See CashPulse in action on your own data. Deploy in 4 to 8 weeks.

We didn't have any real cash flow forecasting for over 10 years. Transformance solved this in a matter of months.

| Manual forecasting | With CashPulse | |

|---|---|---|

| Refresh cadence | ✕Monthly spreadsheet updates | ✓Daily rolling forecasts from live AR data |

| Data source | ✕Historical data only, no forward signals | ✓FX, commodities, weather, payment behaviour |

| Output format | ✕Single-point estimates, no confidence bands | ✓P10, P50, and P90 confidence ranges |

| Entity coverage | ✕Entity-by-entity, no consolidated view | ✓Multi-entity rollup in reporting currency |

| Decision usefulness | ✕Stale by the time it reaches leadership | ✓Always current, always actionable |

GDPR Compliant

End-to-end encryption

Full audit trail

Full audit trail

Cash flow forecasting software predicts future cash position by modelling expected inflows and outflows across AR, AP, and treasury activity. It replaces the monthly Excel forecast that treasury teams rebuild from bank snapshots and aging reports.

AI forecasts from live, processed AR data rather than ERP snapshots. CashPulse knows which invoices will be paid because ClearMatch matched them, which are disputed because ClaimIQ flagged them, and which have promise-to-pay dates because CollectPulse recorded them. Traditional tools forecast from aging buckets and bank balances.

Accuracy depends on data volume and customer payment history. Predictions tighten as the system accumulates resolution patterns. Forecasts are shown with confidence bands so treasury teams see the uncertainty, not a single deceptive number.

Yes. Filter forecasts by legal entity, region, or reporting currency. Each entity's forecast reflects its own customer payment behaviour, not a global average. Critical for multi-entity enterprises operating across dozens of countries.

CashPulse connects to SAP, Oracle, NetSuite, and Microsoft Dynamics. It can feed forecasts back into existing treasury tools or stay self-contained. AR data flows from the other Transformance products directly.

CashPulse goes live in 2 to 4 weeks for the first 13-week forecast, then 4 to 8 weeks full rollout. Weeks, not quarters. The forecast quality improves week-over-week as Vero learns your payment seasonality. Standalone deployment is possible but the signal is cleaner when ClearMatch or CollectPulse is upstream.

Yes. Scenarios are action-linked. If we accelerate collections on the top 20 overdue accounts, how does that change the 30-day forecast? The scenarios connect directly to actions your team can execute, not abstract parameter sliders.

Yes. Deployment runs inside your VPC. Forecast data never leaves your cloud boundary. The platform meets ISO 27001 standards and every forecast change is logged.

CashPulse builds a unified net cash position curve from real AR data (matched payments, active disputes, promise-to-pay dates) and real AP data (committed POs, payroll, tax schedules, contracts). Each entity's flow is netted at the legal-entity level with intercompany flows eliminated. Treasury teams see net cash, not gross inflows.

Legacy platforms run a single auto-regressive model for every customer and every horizon. That works for short stable cycles but loses signal mid and long term, and it treats every variable in isolation. It cannot ingest external factors like FX rates, commodity prices, weather, or harvest cycles that materially shift when customers pay. CashPulse uses a multi-architecture engine that picks the right model per portfolio and horizon. Auto-regressive runs only where it actually fits. Mid-horizon behaviour-driven forecasting uses multi-dimensional ML pattern matching with persistent memory. Long-cycle, multi-entity portfolios with FX or commodity exposure run on a deep learning architecture purpose-built for multi-horizon time series, with quantile outputs and external signal ingestion as first-class inputs.

As of 2026, customers report above 90% accuracy out to 90 days, measured as MAPE on the rolling P50 forecast against actual payment outcomes as invoices close. CashPulse tracks per-horizon accuracy, forecast bias, and per-customer hit rate, and rebuilds the model when accuracy drops below threshold.

Every forecast ships with three lines: best-case (P90), expected (P50), and risk-adjusted (P10). Plan against P10 for liquidity floors and covenant compliance, against P50 for working capital decisions, and against P90 for upside scenarios like early-payment discounts. Stress-test by adjusting external inputs and watch the band move.

Most enterprises deploy with around 3 years of payment history. Stable portfolios can deploy on as little as 1 year. Volatile or seasonal businesses benefit from up to 5 years. For portfolios with smaller scope or less history, CashPulse runs multi-dimensional ML pattern matching instead of the deep learning architecture. Even at the lower data end, accuracy beats legacy auto-regressive forecasting.

See CashPulse in action with your own AR and AP data. First forecast live in days.