In This Article

- Introduction: What is Order-to-Cash?

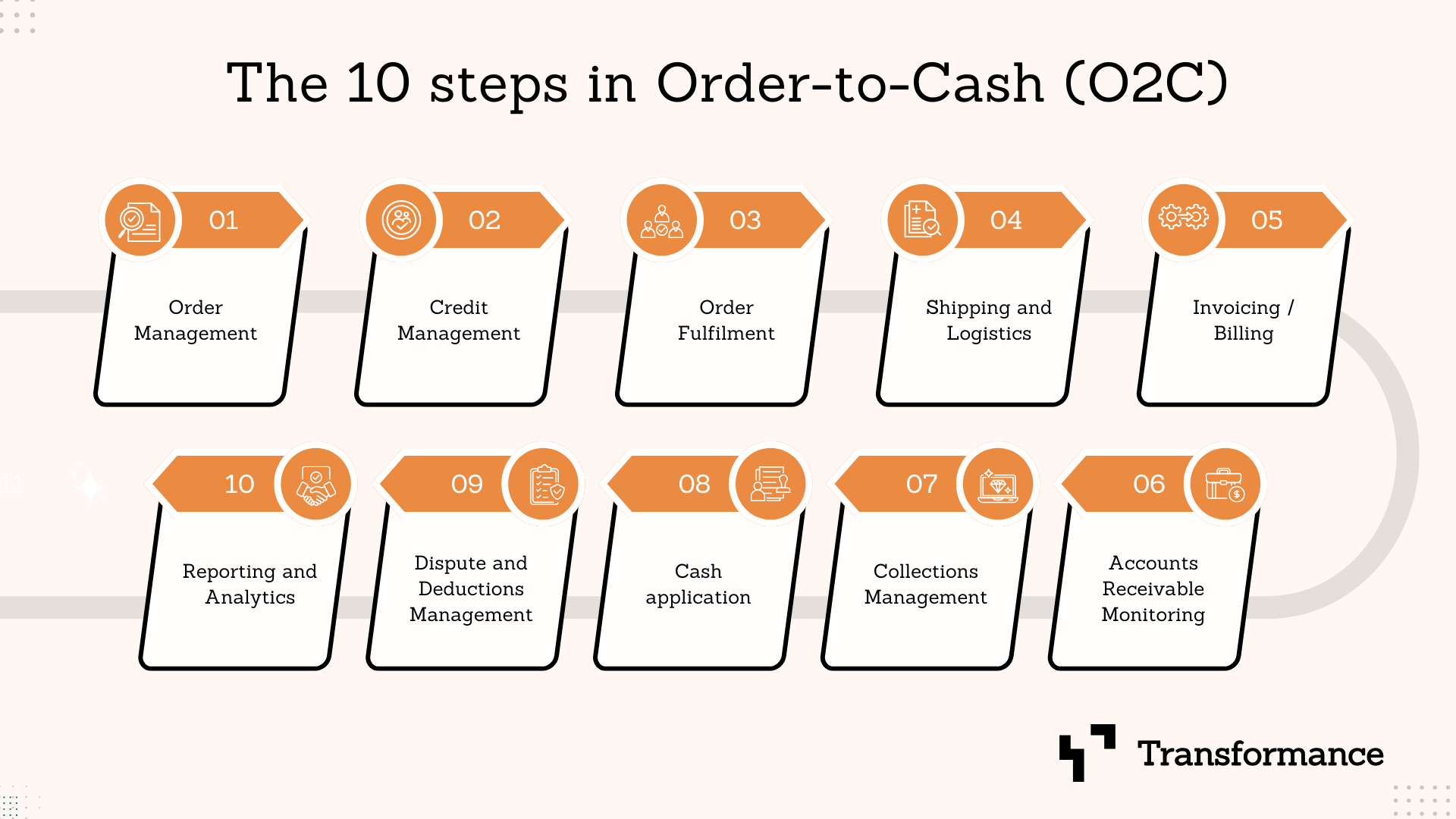

- 1. Order Management

- 2. Credit Management

- 3. Order Fulfillment

- 4. Shipping & Logistics

- 5. Invoicing / Billing

- 6. Accounts Receivable Monitoring

- 7. Collections Management

- 8. Cash Application

- 9. Dispute & Deductions Management

- 10. Reporting & Analytics

- FAQ about O2C

Introduction: What is Order-to-Cash?

Order-to-cash is the lifeblood of any revenue-generating business. It represents the full journey of a transaction: a customer places an order, the business fulfills it, issues an invoice, receives payment, and updates its financial records. While the definition sounds simple, execution rarely is. In large organizations, O2C often spans multiple departments and technology platforms including ERP systems, CRM tools, warehouse management systems, shipping portals, and banking interfaces that do not always speak the same language.

Why does O2C matter? Because it is the direct engine of cash flow. Inefficient O2C processes extend days sales outstanding (DSO), lock up working capital, and reduce liquidity. Independent benchmarks show that top-performing companies run significantly faster O2C cycles than industry peers, freeing up millions in cash that can be reinvested.AI-native automation is redefining how organizations run O2C.

Even in companies with strong ERP implementations, manual interventions still creep in. Staff often key in order data from emails, reconcile delivery notes, check credit limits, or chase overdue payments. These tasks consume hours of staff time and introduce the risk of human error. The result is delayed cash flow, higher DSO, more disputes, and an increased burden on finance teams.

The impact can be significant: a Deloitte study found that improving AR processes by just 5 days can release up to 3% of annual revenue in working capital.

AI is changing that reality. With intelligent document processing, rules-based workflow routing, predictive analytics, and human-in-the-loop validation, AI-native automation platforms can take on the bulk of O2C’s repetitive work. Transformance AI specializes in this space, offering secure, enterprise-grade, AI-driven process automation that integrates directly with existing systems without compromising data security. In highly regulated industries, this means faster, more accurate O2C cycles while maintaining compliance and control. Whether it is auto-validating orders from unstructured emails, detecting credit risk mid-transaction, or matching payments to invoices with 90 percent automation, AI brings speed and precision that legacy tools cannot match.In this blog, we break down each of the 10 steps in the O2C cycle.

For every step, we will outline its purpose, the most common pain points, and how Transformance AI can help using real automation use cases and proof from client results.

1. Order Management

What it is

Order management is the process of capturing, validating, and initiating customer orders. It is the first link in the O2C chain, and its accuracy sets the tone for everything that follows. Orders can arrive through a variety of channels such as email, online portals, EDI feeds, or even scanned paper forms. Once received, the order must be validated against customer records, product availability, and agreed pricing before moving to fulfillment.

Frequent challenges

- Manual entry of order details from emails or PDFs into the ERP, creating scope for errors.

- Mismatches between what sales teams submit and what the ERP or CRM has on record.

- Orders stalling in approval queues because routing rules are unclear or handled manually.

- No real-time validation, leading to late discovery of missing information or incorrect terms.

How Transformance AI can help

- AI-driven data extraction: Captures order details from PDFs, emails, or EDI feeds and posts them directly to the ERP.

- Automated data validation: Cross-checks orders against customer master data, product catalogs, and pricing tables to catch mismatches instantly.

- Rule-based routing: Sends validated orders to the correct fulfillment or approval team without manual intervention.

Fact: According to PwC, companies that digitize order processing can reduce cycle times by up to 40% while lowering processing costs by 30–50%.

2. Credit Management

What it is

Credit management ensures that orders are only processed for customers who meet agreed payment terms and credit risk thresholds. It involves assessing a customer’s financial stability, setting appropriate credit limits, and monitoring for changes that might impact payment reliability.

Frequent challenges

- Manual credit reviews that slow order approvals.

- Incomplete or outdated credit data.

- Missed detection of mid-order credit risk changes.

- Lack of proactive alerts to sales and finance teams.

How Transformance AI can help

- Automated credit checks: Integrates external credit bureau data with internal payment history to provide instant risk assessments.

- Real-time credit limit updates: Adjusts ERP records automatically to block or release orders based on the latest risk profile.

- Proactive credit alerts: Notifies sales and finance teams when customer credit status changes mid-transaction.

Fact: The OECD reports that poor credit control is a leading factor in 25% of SME failures globally. Automating credit monitoring significantly reduces exposure to high-risk transactions.

3. Order Fulfillment

What it is

Order fulfillment covers the picking, packing, and preparation of goods for shipment. It is the bridge between confirming an order and delivering it to the customer. Effective fulfillment relies on synchronized data across ERP, warehouse management systems, and logistics partners.

Frequent challenges

- Siloed systems leading to delays in order status updates.

- Inventory shortfalls discovered after orders are confirmed.

- No streamlined handling of partial shipments or backorders.

- Difficulty identifying fulfillment exceptions early.

How Transformance AI can help

- Cross-system status reconciliation: Pulls data from ERP, WMS, and third-party logistics portals to detect delays or discrepancies.

- Inventory shortage alerts: Flags low stock before an order is confirmed to avoid fulfillment delays.

- Automated backorder workflows: Orchestrates partial shipments and manages follow-up actions without manual coordination.

Fact: A McKinsey & Company study found that digitally enabled fulfillment can improve order accuracy by 15–30% and reduce lead times by up to 50%.

4. Shipping & Logistics

What it is

Shipping and logistics manage the movement of goods from the warehouse to the customer. This step ensures orders are delivered on time, at the agreed cost, and in good condition. It also includes tracking carrier performance and resolving delivery-related issues.

Frequent challenges

- Freight overbilling compared to contracted rates.

- Incomplete or delayed shipment data.

- No consolidated view of carrier performance metrics.

- Difficulty matching delivery records to ERP data.

How Transformance AI can help

- Freight cost reconciliation: Compares invoiced freight costs against contracted rates to identify overbilling before payment.

- Shipment-to-order matching: Automatically aligns shipment data with ERP orders and delivery notes for accurate records.

- Carrier performance analytics: Tracks on-time rates, damage claims, and other KPIs in a single dashboard.

Fact: According to the World Bank Logistics Performance Index, organizations that invest in logistics visibility tools can reduce delivery delays by up to 47%.

5. Invoicing / Billing

What it is

Invoicing and billing involve generating accurate invoices based on fulfilled orders or delivered services, then delivering them to customers in the required format. This step is critical for triggering payment and maintaining strong customer relationships.

Frequent challenges

- Manual invoice creation prone to data entry errors.

- Customer-specific formatting requirements for EDI, XML, or PDF.

- Disputes caused by mismatches between invoices and contract terms.

- Delays in sending invoices, which postpone payment cycles.

How Transformance AI can help

- AI-assisted invoice generation: Pulls delivery and order data directly from systems to produce accurate invoices without manual entry.

- Automated format conversion: Outputs invoices in the exact format required by each customer, from EDI to PDF.

- Pre-bill validation: Checks invoice data against contract terms and delivery records to reduce downstream disputes.

Fact: Ardent Partners research shows that automated invoicing can cut invoice processing costs by 60–80% and reduce billing errors by up to 37%.

6. Accounts Receivable Monitoring

What it is

Accounts receivable (AR) monitoring tracks the status of outstanding invoices to ensure timely payment. It provides visibility into customer payment behavior and helps finance teams prioritize follow-ups based on risk and aging.

Frequent challenges

- Limited real-time visibility into overdue invoices.

- Manual tracking of payment statuses across multiple systems.

- Difficulty identifying high-risk accounts early.

- Inconsistent follow-up schedules.

How Transformance AI can help

- Real-time AR dashboards: Consolidates ERP and bank data to display up-to-date payment status and aging.

- Automated overdue alerts: Notifies teams when invoices cross key aging thresholds.

- High-risk account tagging: Flags customers with repeated late payments for proactive follow-up.

Fact: A Deloitte working capital study found that companies actively monitoring AR can reduce overdue payments by up to 33% within one fiscal year.

7. Collections Management

What it is

Collections management is the process of securing payment for overdue invoices. It involves prioritizing accounts for follow-up, choosing the right communication method, and escalating when necessary to recover outstanding amounts.

Frequent challenges

- Inefficient prioritization of overdue accounts.

- Generic, non-targeted reminder communications.

- Late initiation of collection activities.

- Limited tracking of collection outcomes.

How Transformance AI can help

- AI-prioritized outreach sequencing: Ranks overdue accounts based on payment likelihood to guide collection efforts.

- Automated, personalized reminders: Sends tailored messages to each customer using their payment history and behavior.

- Early risk-triggered outreach: Initiates follow-up before invoices become severely overdue.

Fact: The World Bank notes that proactive collections strategies can improve recovery rates by up to 25%, particularly in markets with longer payment cultures.

8. Cash Application

What it is

Cash application matches incoming payments to the correct open invoices in the ERP. Accurate and timely matching keeps accounts receivable up to date, reduces unapplied cash, and speeds up financial reporting.

Frequent challenges

- Short payments, overpayments, and multiple invoices in one payment.

- Manual matching that consumes significant staff time.

- Missing or incomplete remittance details.

- Delays in posting matched payments to ERP.

How Transformance AI can help

- AI-driven payment matching: Links bank statement lines to open invoices, even with complex remittance scenarios.

- Auto-posting to ERP: Updates financial records once match confidence reaches set thresholds.

- Automated remittance retrieval: Collects payment details from portals and emails to boost match rates.

- Case in point: A Transformance client reached 90% automation in claims matching, saving €60–80k annually.

Fact: AFP research found that organizations with high cash application automation achieve 70% faster payment posting and 80% fewer unapplied payments.

9. Dispute & Deductions Management

What it is

Dispute and deductions management handles situations where customers pay less than the invoiced amount or raise claims related to product quality, shipping, or contractual terms. It requires gathering supporting documentation, validating claims, and resolving them efficiently.

Frequent challenges

- Fragmented data across ERP, CRM, and third-party portals.

- Long resolution cycles that delay cash recovery.

- Lack of standardized root cause tracking for recurring issues.

- Minimal visibility for stakeholders into dispute status.

How Transformance AI can help

- End-to-end claims reconciliation: Integrates data from ERP, CRM, and portals to centralize all dispute information.

- Automated backup retrieval: Gathers required documentation for faster resolution.

- Root cause categorization: Identifies patterns to support upstream process fixes.

- Case in point: A global confectionery company used Transformance AI to automate 90% of claims processing, improving AR by over €1M.

Fact: EY research shows that structured dispute management processes can cut resolution times by up to 40%, directly improving cash recovery rates.

10. Reporting & Analytics

What it is

Reporting and analytics measure the performance of the entire O2C process. They help finance and operations teams track KPIs, identify bottlenecks, and uncover trends that can guide strategic improvements.

Frequent challenges

- Data silos preventing a complete O2C view.

- Delays in generating reports across multiple systems.

- Limited ability to detect anomalies or emerging risks.

- High reliance on IT for custom report creation.

How Transformance AI can help

- Cross-O2C KPI dashboards: Consolidates data on DSO, dispute rates, match rates, and automation coverage in real time.

- AI-based anomaly detection: Spots unusual patterns in revenue, deductions, or payment behavior.

- Self-service reporting builder: Empowers finance teams to create custom reports without IT intervention.

Fact: KPMG reports that companies using advanced analytics in O2C improve forecast accuracy by up to 25% and reduce working capital by 15–20%.

Conclusion: What is Order-to-Cash?

Order-to-cash is one of the most important processes in any business because it directly determines how quickly revenue turns into cash. Every day shaved off the O2C cycle can release working capital back into the business, reduce borrowing costs, and improve customer satisfaction. Yet, in many organizations, inefficiencies in data capture, manual workflows, and siloed systems hold back performance.

AI-native automation is the path forward. By applying intelligent data capture, automated validation, rules-based routing, and predictive analytics, companies can accelerate their O2C cycles without sacrificing accuracy or compliance. Transformance AI offers a secure, enterprise-grade platform that integrates seamlessly with existing ERP, CRM, and financial systems, giving finance leaders complete control and visibility from order entry through final reporting.

Our clients have achieved measurable results, including €1M improvements in accounts receivable and thousands of hours saved annually in manual processing. Whether it is auto-matching payments with 90% accuracy or reducing claims resolution time by days, the proof is in the outcomes.

Fact: A McKinsey analysis found that organizations with top-quartile O2C performance achieve up to 3x higher cash flow velocity than median performers.

FAQ about O2C

What is meant by order-to-cash?

The complete process from receiving a customer order to delivering goods or services and collecting payment. For a deeper dive, see our Order-to-Cash automation guide.

Are O2C and AR the same?

No. Accounts receivable is one component of O2C, focused on tracking and collecting payments

What are the steps in the order-to-cash process?

Order management, credit management, order fulfillment, shipping and logistics, invoicing, accounts receivable monitoring, collections, cash application, dispute management, and reporting.

What is the difference between O2C and P2P?

O2C covers the customer sales-to-payment cycle, while procure-to-pay (P2P) manages supplier purchases-to-payment. Learn more about automation in finance workflows.

Is O2C accounts receivable?

No. Accounts receivable is part of O2C but the cycle includes upstream order capture, fulfillment, and billing.

Why is order-to-cash important?

It impacts cash flow, working capital, and customer experience. Efficient O2C improves liquidity and profitability. The World Bank has identified payment delays as a significant barrier to SME growth worldwide.

What is the O2C cycle time?

The duration from order receipt to payment collection. Shorter cycle times lead to faster cash flow.

What are the risks of O2C?

Common risks include data errors, shipment delays, payment disputes, and poor process visibility.

What is the billing process in O2C?

Generating accurate invoices from order or delivery data, validating against contract terms, and sending them to customers promptly.

How do you explain O2C in an interview?

It is the end-to-end process of taking a customer order, fulfilling it, billing the customer, and collecting payment - with each step impacting cash flow and customer satisfaction.

Frequently Asked Questions

What is invoice-to-cash automation software?

Invoice-to-cash (I2C) automation software covers the steps from invoice generation through payment receipt and GL posting — billing, dispute management, collections, cash application, and reconciliation in one platform. It differs from "cash application software" (which only handles the matching step) and from "AR automation" (broader catch-all). Strong I2C platforms in 2026 use AI for predictive collections, auto-matching of remittances, and ERP-native posting. Most enterprises evaluate I2C tools alongside their ERP refresh because I2C and the order side of order-to-cash share the same customer master data.