Transformance is the AI-native execution layer for accounts receivable: built on vision language models that understand remittance documents natively, not OCR + regex templates that break when customer formats change. This guide covers where AI creates real ROI in enterprise finance, how to evaluate solutions, and what separates genuine AI-native platforms from legacy tools wearing an AI marketing layer.

Key Takeaways

- AI in finance and accounting reduces DSO by 8-15 days and automates 60-80% of routine AR touches within 90 days of deployment

- The application of AI in finance spans cash application, collections, deductions management, and cash forecasting, not just analytics dashboards

- Legacy platforms built on OCR + regex + RPA require weeks of template configuration per new remittance format; AI-native platforms handle new formats on first contact, without configuration

- Governance design is the primary implementation bottleneck: define approval hierarchies before deploying autonomous AI agents

- Full rollout for a mid-market enterprise takes 4-8 weeks, compared to 3-6 months for incumbent AR platforms

In This Article

- What Is AI in Finance?

- Why Does AI in Finance Matter for Enterprise Finance?

- How Is AI Transforming Order-to-Cash?

- What Are the Key Challenges in AI Finance Deployment?

- How Do You Evaluate AI Finance Solutions?

- What Does Real-World AI in Finance Actually Deliver?

- Build vs. Buy: The Honest Framework

What Is AI in Finance?

AI in finance is the application of machine learning, vision language models, generative AI, and autonomous agents to automate, predict, and act on financial processes, replacing rules-based manual workflows with systems that learn from data and improve over time.

The definition covers a wide range. At one end: simple ML models that flag anomalies in expense reports. At the other: autonomous AI agents that read a remittance advice from an email attachment, match it to 40 open invoices across multiple currencies, and post the journal entry to SAP without human intervention. According to McKinsey’s 2025 State of AI report, 78% of organizations now use AI in at least one business function, with finance ranking among the top three adoption areas. The question is no longer whether to use AI in finance; it’s which processes to automate first and how to evaluate the tools doing it.

Why Does AI in Finance Matter for Enterprise Finance?

Finance teams sit on some of the most structured, high-volume, rule-bound data in any enterprise. That makes them ideal candidates for AI automation and, historically, resistant to it: the ERP is the system of record, changes require IT sign-off, and errors carry regulatory consequence.

The cost of not automating is measurable. According to the Institute of Finance & Management (IOFM), companies with fully manual AR processes average 42 days sales outstanding (DSO), compared to 32 days for companies using AI-assisted automation. That 10-day gap represents real working capital tied up in unpaid invoices.

According to a 2024 Hackett Group benchmark, top-performing finance organizations process 4.6x more transactions per FTE than median peers, with AI as the primary driver. The ROI story has shifted from efficiency to coverage: AI doesn’t just save time on the tasks your team gets to. It actions every invoice, every deduction, every follow-up, including the ones your team would never reach.

The critical distinction for 2026 is between AI that assists and AI that executes. Dashboards and analytics tell you cash is short. Execution-layer AI triggers the collection call, matches the remittance, and posts the entry. Finance leaders who’ve made the transition describe it consistently: “We stopped managing data and started managing exceptions.”

How Is AI Transforming Order-to-Cash?

Order-to-cash (O2C) is where the AI in finance and accounting opportunity is most concrete. The process runs from invoice creation to cash receipt, and most bottlenecks sit in the middle: unprocessed remittances, unresolved deductions, and overdue invoices that don’t get followed up because the team is already at capacity.

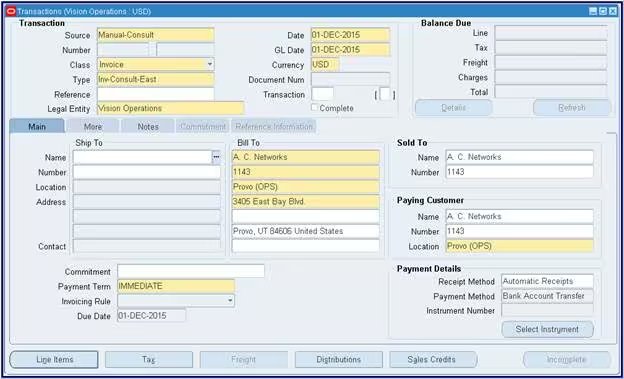

Cash Application: From Document to GL Entry

The traditional cash application workflow: a remittance advice arrives as a PDF, a bank file drops in MT940 format, and an AR analyst spends 30-45 minutes cross-referencing them against open invoices in SAP, reconciling partial payments, and posting the result. Multiply that by 200 payments per week and the math collapses.

AI cash application replaces the first 80-90% of that workflow. Platforms built on vision language models read the remittance advice as a document, extracting amounts, invoice references, and payment dates without any template configuration. This matters because remittance formats vary by customer: a retailer in Germany sends a structured Excel export; a distributor in Spain sends a scanned PDF with hand-typed references; a US subsidiary sends a portal download with non-standard column headers. Template-based OCR tools require manual configuration for each format. VLM-based extraction handles all of them on first contact.

ClearMatch, Transformance’s cash application module, uses a five-layer matching process: deterministic rules handle the majority of matches, ML-pattern matching resolves timing differences and payment splits, and an AI agent investigates the edge cases that legacy tools push straight to the human queue. Match rates start at ~85% on day one and improve to 95%+ within 90 days as MemoryMesh accumulates institutional knowledge about each customer’s payment patterns.

For how this works in SAP environments specifically, SAP Cash Application: Complete Guide covers integration architecture and typical deployment timelines.

Collections: From Worklists to Autonomous Action

Most collections tools give AR teams a prioritized worklist of overdue accounts and leave execution to humans. The coverage problem compounds over time: manual teams action 30-40% of overdue invoices in any given week.

CollectPulse changes the coverage equation. Automated dunning sequences handle first and second touches without human involvement. AI calling agents contact overdue accounts, capture promise-to-pay dates, log dispute reasons, and write outcomes back to the system automatically. Promise-to-pay tracking then schedules verification follow-ups and feeds broken promises back into priority scoring.

The throughput difference is significant: AI calling agents process 15-20 calls per hour, compared to 15-20 calls per day for a human collector. The result is 100% of overdue invoices actioned within 24 hours. No invoice sits untouched because a collector had a full queue or was on vacation.

The multilingual dimension matters for international operations. A shared service center in Warsaw handling collections for Italy, France, and Spain normally requires native speakers for each market. AI calling agents that operate in 70+ languages remove that constraint entirely, letting a small team run multilingual collections without adding headcount.

Deductions Management: From Backlog to Investigation

Trade deductions are the perennial bottleneck for CPG, FMCG, and retail-facing businesses. Retailers deduct against invoices for dozens of reasons: trade promotions, pricing discrepancies, shortages, damaged goods, early payment discounts. Validating each one requires cross-referencing the deduction memo against promotional agreements, proof of delivery, pricing records, and historical resolutions.

The AI breakthrough here is graph-based cross-document retrieval. Instead of an analyst searching six systems sequentially over several hours, an AI investigation engine constructs a knowledge graph of relationships between deductions, invoices, promotional agreements, and delivery records, then traces the connections simultaneously. Valid deductions are auto-settled. Invalid ones generate a dispute package automatically, ready for analyst review.

Industry data puts 5-10% of trade deductions as invalid, according to IOFM benchmarks. For a company processing 5,000 monthly deductions, recovering even 5% represents six figures in annual write-off reversal that was previously accepted as cost of doing business.

The Claims Management Software: Complete Guide covers the full evaluation framework for deductions and claims tools.

Cash Forecasting: From ERP Snapshots to Processed Data

Most cash forecasting tools pull from ERP snapshots: what does the system show for open AR? The problem is that ERP data includes unprocessed remittances, unresolved deductions, and invoices in active dispute. Forecasting on unprocessed data produces unreliable forecasts.

AI-driven forecasting built on top of processed AR data is structurally more accurate. When the upstream cash application and collections processes have already matched payments, logged promise-to-pay dates, and flagged disputed invoices, the forecast knows which invoices will pay, when, and what’s at risk. According to a 2024 PwC Global Treasury Survey, finance teams using real-time AR data as their forecasting foundation report 30-40% improvement in 30-day forecast accuracy.

For a detailed look at short-term forecasting methodology, 13 Week Cash Flow: What Finance Teams Need covers the rolling forecast approach and where AI improves signal quality.

What Are the Key Challenges in AI Finance Deployment?

The technology challenges are smaller than you’d expect. The governance and change management challenges are larger.

Governance: Who Approves What?

Autonomous AI agents need a clear approval hierarchy before you deploy them. An agent that sends dunning emails is different from one that posts journal entries to the ERP. Define these levels before go-live:

- Read-only queries: AI retrieves and displays data without human approval

- Recommendations: AI suggests actions; human reviews and confirms each one

- Execution (external): AI sends communications (dunning emails, collection calls) under a pre-approved policy, without per-instance approval

- ERP posting: Human-in-the-loop sign-off always; schema validation before anything touches the system of record

A platform with a well-designed approval hierarchy makes this governance structure explicit and auditable. If a vendor can’t show you how each action type is gated and logged, that’s a meaningful red flag.

Data Quality: The Input Problem

AI models are only as good as the data they receive. If your AR data is fragmented across the ERP, a collections tool, and individual team members’ spreadsheets, AI agents will make worse decisions than a human analyst with full context.

The practical answer: start with your highest-volume, most structured input (bank statements and standard remittance formats), let the system build institutional memory on clean data, and then expand to more complex cases. Don’t try to automate everything on day one.

Change Management: The Analyst’s Role Shift

The most common implementation failure isn’t technical. It’s cultural. AR analysts who’ve built expertise in deduction investigation or customer relationship management often perceive AI automation as a threat.

The reframe that works: AI handles the repetitive first 80% (data extraction, initial matching, routine follow-up) so the analyst focuses on the 20% that requires real judgment (disputed claims, escalated negotiations, exception handling). Teams that communicate this shift early, involve analysts in configuration, and track metrics showing individual contribution see significantly higher adoption.

Explainability: Can You Audit the Decision?

Regulators and auditors increasingly require finance teams to explain AI decisions. Why was this payment matched to that invoice? Why was this deduction classified as invalid? Why was this customer flagged for escalation?

Explainable AI in finance is a design requirement, not an afterthought. For a detailed look at what explainability means for AR and accounting teams in practice, Explainable AI in Finance: Why It Matters covers the regulatory drivers and what good audit trails actually look like.

How Do You Evaluate AI Finance Solutions?

The AI in finance market is flooded with vendor claims. Every incumbent has added “AI-powered” to its marketing. Evaluating what’s real requires testing specific capabilities against specific requirements. Here are 7 criteria that separate genuine AI-native platforms from legacy tools with AI marketing veneers:

- Document understanding without templates. Ask the vendor to process three remittance formats they’ve never seen. Template-based OCR tools require configuration time. VLM-based tools handle them correctly on first contact. This test takes 30 minutes and is the fastest differentiator between real AI and marketing AI.

- Match rate trajectory over 90 days. Any vendor can quote an 85% Day 1 match rate. Ask for their rate at 30, 60, and 90 days. A system with persistent memory should improve measurably as it learns your customers’ payment patterns. Transformance’s MemoryMesh drives match rate improvement from ~85% to 95%+ within 90 days, with no manual retraining. Flat match rates over that period indicate a static rules engine, not learning AI.

- Deployment timeline with specifics. First payments matched in days. Full rollout (ERP integration, remittance capture, deduction workflows) in 4-8 weeks. Any vendor quoting 6+ months for initial deployment is running a professional services engagement disguised as a product sale.

- Approval hierarchy and complete audit trail. Can you see every AI action, what triggered it, and who approved it? Can you restrict certain action types by user role? Finance AI without a complete audit trail is a liability, not an asset.

- ERP posting validation. Does the platform validate journal entries against your chart of accounts and posting rules before they touch the ERP? Zero-error posting requires schema validation at the handoff point, not after.

- Multilingual and multi-entity support. For enterprises operating across multiple countries, the collections agent needs to work in local languages and the forecast needs to consolidate by legal entity and reporting currency. Many mid-market vendors fall short here.

- Persistent institutional memory. Does the system learn from past resolutions? Does it remember that Customer X always pays 5 days late in Q4, or that a specific retailer codes seasonal promotions under a non-standard category? A stateless AI starts from zero each day. Persistent memory compounds your institutional knowledge over time and becomes an organizational asset that survives staff turnover.

For a look at the ML layer that powers payment behavior prediction specifically, ML Payment Prediction: Finance Guide covers how payment probability models are trained and applied in an AR context.

What Does Real-World AI in Finance Actually Deliver?

Finance leaders want concrete numbers, not vague case study vignettes. Here’s what benchmarks and deployment data show:

DSO reduction: Companies with fully automated AR processes report DSO 8-15 days lower than manual-first peers, according to Hackett Group benchmarks. The mechanism is 100% coverage of overdue invoices, compounded over time, versus 30-40% for manual teams.

Cash application accuracy: VLM-based extraction achieves 99.7% accuracy on structured remittance data and 94.9% accuracy across document types, without template configuration. Traditional OCR + regex approaches require 2-6 weeks of template setup per new remittance format and degrade silently as customer formats change.

Collections throughput: AI calling agents process 15-20 calls per hour versus 15-20 calls per day for a human collector. Promise-to-pay capture rates increase 3x with automated follow-up sequences.

Deductions recovery: At a benchmark 5-10% invalid rate on trade deductions, a company processing 5,000 monthly deductions recovers 250-500 invalid claims per month through automated investigation. At an average claim value of €2,000, that’s €500K-€1M in annual recovery previously written off as the cost of doing business.

Forecast accuracy: Finance teams using processed AR data as the basis for short-term forecasting report 30-40% improvement in 30-day forecast accuracy, according to the 2024 PwC Global Treasury Survey.

Build vs. Buy: The Honest Framework

Finance leaders asking how to use AI in finance for the first time often land on the same question: is it faster to build internally using off-the-shelf models and proprietary data? The honest answer is that building the AI layer is not the constraint. The constraints are ERP integration depth, governance architecture, institutional knowledge capture, and ongoing maintenance as both ERPs and customer payment behavior evolve.

An in-house ML model can predict payment probability. But connecting it to SAP’s GL posting rules, validating journal entries before they touch the ledger, and capturing 18 months of deduction resolution history as compounding institutional memory, while maintaining everything as your ERP version updates: that’s the actual engineering cost. Most finance IT teams lack the bandwidth or domain expertise to sustain it indefinitely.

The build argument makes sense for highly idiosyncratic processes where no vendor supports specific regulatory or format requirements. For order-to-cash automation, purpose-built platforms with domain-specific training data and pre-built ERP connectors reach value faster and maintain it more reliably than in-house builds.

The practical test: if the project champion behind the internal build leaves the company, can your IT team maintain the custom cash application system indefinitely? If the answer is uncertain, that’s your answer on build vs. buy.

Conclusion

The technology for AI in finance exists and works. Vision language models read complex documents accurately. ML models predict payment behavior reliably. Autonomous agents execute collections workflows at scale, in 70+ languages. The hard part is deploying it with the right governance, the right ERP integration depth, and the right change management in place.

Finance teams that get the most from AI don’t buy a platform and wait for results. They start with their highest-volume, most structured process, define their approval hierarchy before go-live, and expand as the system accumulates institutional memory. Transformance deploys the full order-to-cash automation stack in 4-8 weeks, with first payments matched in days.

The AI in finance industry is past pilot projects and into production deployments. The teams that started 18 months ago are running 95%+ auto-match rates and 8-15 day DSO reductions. The teams evaluating now will reach those numbers within 90 days of deployment. The only question worth asking is which process to start with.

Frequently Asked Questions

What is AI in finance?

AI in finance is the application of machine learning, vision language models, and autonomous agents to automate, predict, and act on financial processes including cash application, collections, deductions management, and cash forecasting. It ranges from ML models that predict payment timing to autonomous agents that execute collection calls in 70+ languages without human intervention.

What are the main applications of AI in finance and accounting?

The main applications of AI in finance and accounting fall into four categories: cash application automation (matching payments to open invoices and posting to ERP), collections automation (prioritizing overdue accounts and executing dunning sequences autonomously), deductions management (identifying, classifying, and investigating short payments), and cash forecasting (predicting inflows using real-time AR data rather than static ERP snapshots). Each application reduces DSO and frees AR teams to focus on exceptions and negotiations that require human judgment.

How long does it take to deploy AI in finance?

For purpose-built AR automation platforms, first payments can be matched within days of initial configuration. Full rollout, including ERP integration, remittance capture, and deduction workflows, typically takes 4-8 weeks. This compares to 3-6 months for legacy AR platforms, and 18-24 months to reach meaningful value from SAP’s native cash application module.

What is the ROI of AI in finance for AR teams?

Finance teams deploying AI in order-to-cash typically see DSO reduction of 8-15 days within 90 days of deployment. Additional ROI drivers include 60-80% of routine AR touches automated by AI agents, 100% coverage of overdue invoices compared to 30-40% for manual teams, and recovery of 5-10% of trade deductions previously written off as invalid. According to Hackett Group benchmarks, top-performing finance organizations process 4.6x more transactions per FTE than median peers.

How do I use AI in finance without creating compliance risks?

Define a clear approval hierarchy before deploying autonomous agents: which action types can AI execute under pre-approved policy (sending dunning emails), which require per-instance human review (dispute packages), and which always need explicit sign-off (ERP journal entries). Every action should generate a complete audit trail. Platforms that cannot demonstrate this governance architecture out of the box should not reach your short list.

What is the difference between AI-native and AI-enabled finance platforms?

AI-native platforms were built from the ground up on machine learning, vision language models, and autonomous agent architecture. AI-enabled platforms are legacy tools built on OCR + regex + RPA stacks, with ML modules added on top. The practical difference: AI-native platforms handle new document formats without template configuration, improve match rates automatically through persistent memory, and deploy in weeks. AI-enabled platforms require template setup per remittance format, deliver static match rates, and take months to implement.

Can AI in finance work with SAP, Oracle, and NetSuite?

Yes. Purpose-built AI finance platforms connect to SAP (including S/4HANA and ECC environments), Oracle, NetSuite, and Microsoft Dynamics via native ERP connectors. The critical integration point is the posting layer: every journal entry should be validated against the chart of accounts and posting rules before touching the ERP, with human sign-off required. Bank statement ingestion typically supports MT940, CAMT.053, and BAI2 formats.

What should a CFO look for in AI finance software?

Seven criteria matter most: document understanding without template configuration, match rate improvement trajectory over 90 days rather than just Day 1 numbers, specific deployment timelines in weeks not months, a transparent audit trail for every AI action, ERP posting validation before anything touches the system of record, multilingual and multi-entity support for international operations, and evidence of persistent institutional memory that improves as the system learns your customers’ payment patterns.